Deutsche Bank is a German multinational investment bank and financial services company based in Frankfurt, Germany. It's dual-listed on both the Frankfurt Stock Exchange and the New York Stock Exchange. The bank offers a range of financial products and services including investment banking, corporate banking, asset management, and private banking to individuals, corporations, and institutions worldwide. Deutsche Bank is one of the largest banks globally and a significant player in the international financial system.

1901: Branch Expansions

In 1901, Deutsche Bank established branches in Dresden and Leipzig, expanding its domestic network.

1908: Largest German Joint-Stock Bank

By the end of 1908, Deutsche Bank was the largest German joint-stock bank by total deposits, with 489 million Marks.

1914: Acquisition of Bergisch-Märkische Bank

In 1914, Deutsche Bank acquired Bergisch-Märkische Bank in Elberfeld, solidifying its presence in the Rhineland's industrial economy.

1919: Purchase of UFA Share

In 1919, Deutsche Bank purchased the state's share of Universum Film Aktiengesellschaft (UFA).

1926: Assistance in Daimler-Benz Merger

In 1926, Deutsche Bank assisted in the merger of Daimler and Benz, playing a role in the creation of the automotive giant.

1928: Formation of Allgemeiner Jugoslawischer Bankverein

In 1928, the Allgemeiner Jugoslawischer Bankverein (AJB) was formed.

1929: Merger with Disconto-Gesellschaft

In 1929, Deutsche Bank merged with Disconto-Gesellschaft and rebranded as Deutsche Bank und Disconto-Gesellschaft, also called DeDi-Bank.

1930: Dominant Position

By 1930, Deutsche Bank & Disconto-Gesellschaft maintained a dominant position in the banking sector with 4.8 billion Reichsmarks in total deposits.

1931: Government Ownership Increase

In the crisis summer of 1931, the Deutsche Golddiskontbank, a subsidiary of the Reichsbank, acquired 35 percent of DeDi-Bank's equity, bringing total government ownership to 38.5 percent.

1934: Dismissal of Jewish Management Board Members

In 1934, Deutsche Bank dismissed its three Jewish management board members, Oscar Wassermann, Theodor Frank, and Georg Solmssen, as it became integrated into Nazi power structures.

1935: Reprivatization Begins

In 1935, the Nazi government began to re-privatize Deutsche Bank.

1937: Name changed back to Deutsche Bank

In 1937, Deutsche Bank changed its name back from Deutsche Bank und Disconto-Gesellschaft.

1937: Name Change

In 1937, after a period as Deutsche Bank und Disconto-Gesellschaft, the bank's name reverted back to Deutsche Bank.

March 1938: "Friendship Agreement" with Creditanstalt and Arrest of Louis de Rothschild

In March 1938, Creditanstalt-Bankverein was coerced to enter a "friendship agreement" with Deutsche Bank, leading to Deutsche Bank securing a presence on its board and the arrest and imprisonment of Creditanstalt executive Louis de Rothschild.

1938: Acquisition of Mendelssohn & Co.

In 1938, Deutsche Bank acquired Mendelssohn & Co., marking another transformative acquisition in its history.

1938: Dismissal of Last Jewish Supervisory Board Member and Acquisition of Mendelssohn & Co.

In 1938, Deutsche Bank dismissed its last Jewish supervisory board member and acquired Jewish-controlled German bank Mendelssohn & Co. under duress.

March 1939: Forcible takeover of Böhmische Union Bank

In March 1939, Deutsche Bank forcibly took over control of the BUB.

1939: Rothschild migrates to U.S.

In 1939, Louis de Rothschild migrated to the U.S.

1940: Dominant shareholder in Allgemeiner Jugoslawischer Bankverein

In 1940, Deutsche Bank became the dominant shareholder in the Allgemeiner Jugoslawischer Bankverein (AJB), with 88 percent held either directly or through Creditanstalt.

April 1942: Deutsche Bank Raises Ownership of Creditanstalt

In April 1942, Deutsche Bank raised its ownership of Creditanstalt to 51 percent by acquiring a block of shares from VIAG.

1942: Purchase of gold from the Reichsbank

Between 1942 and 1944, Deutsche Bank purchased gold from the Reichsbank

October 1944: Confiscation of AJB assets

In October 1944, the assets of the Bankverein AG Belgrad and the Bankverein für Kroatien AG (formerly the AJB) were confiscated by Communist authorities.

1944: Purchase of gold from the Reichsbank

Between 1942 and 1944, Deutsche Bank purchased gold from the Reichsbank

1952: Consolidation into Three Major Banks

In 1952, the regional banks created from the break-up were consolidated into three major banks: Norddeutsche Bank AG, Süddeutsche Bank AG, and Rheinisch-Westfälische Bank AG.

1957: Merger to form Deutsche Bank AG

In 1957, the three major banks (Norddeutsche Bank AG, Süddeutsche Bank AG, and Rheinisch-Westfälische Bank AG) merged to form Deutsche Bank AG, with its headquarters in Frankfurt.

1959: Entry into Retail Banking

In 1959, Deutsche Bank entered retail banking by introducing small personal loans.

1972: "Slash in a Square" Created

In 1972, Deutsche Bank created the world-known blue logo "Slash in a Square" – designed by Anton Stankowski.

1972: Establishment of Fiduciary Services Division

In 1972, Deutsche Bank established its Fiduciary Services Division to provide support to its private wealth division.

1977: Opening of Milan Office

In 1977, Deutsche Bank opened a new office in Milan as part of its international expansion.

1978: Exception to U.S. banking laws

In 1978, Deutsche Bank received an exception to US banking laws.

1986: Acquisition of Banca d'America e d'Italia

In 1986, Deutsche Bank acquired Banca d'America e d'Italia for U$603 million, continuing its international expansion.

November 1989: Assassination of Alfred Herrhausen

On November 30, 1989, Alfred Herrhausen, chairman of Deutsche Bank, was assassinated by the Red Army Faction in Bad Homburg.

1989: Acquisition of Morgan, Grenfell & Co.

In 1989, Deutsche Bank took the first steps toward a major investment banking presence by acquiring Morgan, Grenfell & Co.

1990: Acquisition of Morgan Grenfell

In 1990, Deutsche Bank acquired Morgan Grenfell, further expanding its reach and influence.

1994: Renaming of Acquired Investment Bank

In 1994, the UK-based investment bank Morgan, Grenfell & Co., acquired by Deutsche Bank, was renamed Deutsche Morgan Grenfell.

1995: Expansion into International Investments

In 1995, Deutsche Bank hired risk specialist Edson Mitchell from Merrill Lynch, leading to significant expansion into international investments and money management.

1995: Publication of History Volume

In 1995, Deutsche Bank published a history volume detailing its entanglement with the Nazi dictatorship in an effort to address its past.

November 1998: Acquisition of Bankers Trust

In November 1998, Deutsche Bank acquired Bankers Trust for $10 billion after Bankers Trust suffered losses during the Russian financial crisis.

1998: Acquisition of Bankers Trust

In 1998, Deutsche Bank acquired Bankers Trust, significantly increasing its assets and market presence.

June 1999: Merger to form Deutsche Asset Management

On June 4, 1999, Deutsche Bank merged Deutsche Morgan Grenfell and Bankers Trust to create Deutsche Asset Management (DAM).

December 1999: Contribution to Holocaust Compensation Fund

In December 1999, Deutsche Bank contributed to a US$5.2 billion compensation fund for Holocaust survivors following legal pressure.

1999: Minority Interest in Cassa di Risparmio di Asti

In 1999, Deutsche Bank acquired a minority interest in Cassa di Risparmio di Asti.

1999: Acknowledgement of Involvement at Auschwitz

In 1999, Deutsche Bank publicly acknowledged its involvement at Auschwitz.

1999: Start of sanctions violations

In early 1999, Deutsche Bank began handling US dollar clearing transactions to help evade US sanctions.

1999: FinCEN file leaks

The FinCEN file leaks documented around $1.3 trillion of suspicious transactions through Deutsche Bank between 1999 and 2017.

2001: Eurohypo AG Formed

In 2001, Deutsche Bank merged its mortgage banking business with that of Dresdner Bank and Commerzbank to form Eurohypo AG.

2001: Start of espionage on critics

In 2001, Deutsche Bank started covert espionage on its critics, continuing until 2007.

2002: Josef Ackermann becomes CEO and Scudder Investments purchased

In 2002, Josef Ackermann became CEO of Deutsche Bank and Deutsche Bank strengthened its U.S. presence by purchasing Scudder Investments. In Europe, Deutsche Bank increased its private-banking business by acquiring Rued Blass & Cie.

October 2003: Payment Transaction Agreement with Postbank

On October 1, 2003, Deutsche Bank and Dresdner Bank entered into a payment transaction agreement with Postbank to have Postbank process payments as the clearing center for the three banks.

2005: Acquisition of United Financial Group

In 2005, Deutsche Bank acquired the Russian investment bank United Financial Group.

2005: Sale of Stake in Eurohypo AG

In 2005, Deutsche Bank sold its stake in Eurohypo AG to Commerzbank.

2005: Cartel Activities in Europe

In Europe, Deutsche Bank revealed cartel activities in the period between 2005 and 2016 to regulators to receive immunity.

2006: Inadequate haircut on trades

In 2006 another employee described accounting for the gap option first with a simple 15% "haircut" on the trades as inadequate.

2006: End of sanctions violations

In 2006, Deutsche Bank's handling of US dollar clearing transactions to help evade US sanctions came to an end.

2007: End of espionage on critics

In 2007, Deutsche Bank's covert espionage on its critics concluded. The bank later characterized the incidents as "isolated" in 2009.

October 2008: Stopped modeling the gap option

In October 2008, Deutsche Bank stopped modeling the gap option and just bought S&P put options to guard against further market disruption.

2008: Fines and Settlements

Between 2008 and 2016, Deutsche Bank paid around nine billion dollars in fines and settlements related to wrongdoings across different issue areas.

2008: Scheme to Conceal Bribes

In 2008, Deutsche Bank engaged in a scheme to conceal bribes to foreign officials.

2008: Settlement with US Housing Finance Agency

In 2008, Deutsche Bank had a settlement with the US Housing Finance Agency over similar litigation related to the sale of mortgage-backed securities to Fannie Mae and Freddie Mac.

2008: First annual loss in five decades

In 2008, Deutsche Bank reported its first annual loss in five decades, despite receiving billions of dollars from its insurance arrangements with AIG.

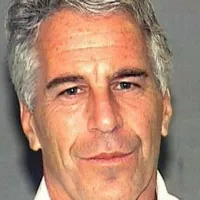

2008: Epstein's guilty plea

In 2008, Jeffrey Epstein pleaded guilty in Florida to soliciting prostitution from underage girls, but Deutsche Bank continued to do business with him.

2008: Trump Sues Deutsche Bank

In 2008, Trump sued Deutsche Bank for $3 billion.

May 2009: Company document described trades as "the largest risk in the trading book"

A company document of May 2009 described the trades as "the largest risk in the trading book".

July 2009: Report finds no systemic misbehavior

In July 2009, Deutsche Bank's law firm Cleary Gottlieb Steen & Hamilton published a report stating that it found no systemic misbehavior.

October 2009: Confirmation from Public Prosecutor

In October 2009, the Public Prosecutor's Office in Frankfurt confirmed the findings of no systemic misbehavior.

2009: Deutsche Bank admits to espionage

In 2009, Deutsche Bank admitted it engaged in covert espionage on its critics from 2001 to 2007.

2009: Deutsche Bank Admits Wrongdoing in the UK

In the UK, Deutsche Bank admitted to wrongdoing for the period 2009–2013 to the Competition and Markets Authority.

2010: Acquisition of Deutsche Postbank

In 2010, Deutsche Bank acquired Deutsche Postbank, continuing its pattern of transformative acquisitions.

2010: Start of Global Laundromat scandal

In 2010, the Global Laundromat scandal began, revealing Deutsche Bank's involvement in a vast money-laundering operation.

2011: Capital Raise Requirement

In 2011, Deutsche Bank AG needed to raise capital of about €3.2 billion as part of a required 9% core Tier 1 ratio after sovereign debt write-down.

2011: Designation as a Systemically Important Bank

In 2011, Deutsche Bank was designated a global systemically important bank by the Financial Stability Board.

February 2012: Co-CEOs Lead Deutsche Bank

Beginning in February 2012, Deutsche Bank has been led by two co-CEOs.

June 2012: Libor scandal uncovered

The Libor scandal, in which Deutsche Bank was involved, was uncovered in June 2012.

2012: Payments for litigation

Since 2012, Deutsche Bank had paid more than €12 billion for litigation, including a deal with U.S. mortgage-finance giants Fannie Mae and Freddie Mac.

2012: Starting of sovereign debt write-down

Starting in mid-2012, Deutsche Bank AG needed to raise capital of about €3.2 billion as part of a required 9% core Tier 1 ratio after sovereign debt write-down.

2013: Accounts opened with Deutsche Bank

From 2013 to 2018, "Epstein, his related entities and his associates" opened over forty accounts with Deutsche Bank.

2013: Fourth quarter loss

In January 2014, Deutsche Bank reported a €1.2 billion pre-tax loss for the fourth quarter of 2013.

2013: Deutsche Bank Admits Wrongdoing in the UK

In the UK, Deutsche Bank admitted to wrongdoing for the period 2009–2013 to the Competition and Markets Authority.

January 2014: Pre-tax Loss Reported

In January 2014, Deutsche Bank reported a €1.2 billion pre-tax loss for the fourth quarter of 2013.

January 2014: Documents released reveal irregularities

On 26 January 2014, William S. Broeksmit released Deutsche Bank documents revealing irregularities, including a $10 billion money laundering scheme.

January 2014: Settlement with US Shareholders

On January 3, 2014, it was reported that Deutsche Bank would settle a lawsuit brought by US shareholders, who had accused the bank of bundling and selling bad real estate loans before the 2008 downturn.

2014: Deutsche Bank raises money for 1MDB

In 2014, Deutsche Bank helped raise $1.2 billion for the 1MDB.

2014: End of Global Laundromat scandal

In 2014, the Global Laundromat scandal concluded, revealing Deutsche Bank's involvement in a vast money-laundering operation.

2014: First annual profit in 6 years

In February 2021, it was reported that Deutsche Bank made a profit of €113 million ($135.6 million) for 2020, the first annual net profit it had posted since 2014.

2014: Supervision by the European Central Bank

In late 2014, Deutsche Bank was designated as a Significant Institution and became directly supervised by the European Central Bank.

April 2015: Deutsche Bank fined for Libor scandal

On 23 April 2015, Deutsche Bank agreed to pay a combined US$2.5 billion in fines for its involvement in the Libor scandal.

June 2015: Co-CEOs Resignation

In June 2015, the then co-CEOs, Jürgen Fitschen and Anshu Jain, both offered their resignations to the bank's supervisory board, which were accepted. Jain's resignation took effect in June 2015.

July 2015: Announcement of Single CEO

In July 2015, Deutsche Bank announced it would be led by one CEO beginning in 2016.

July 2015: Appointment of John Cryan

The appointment of John Cryan as joint CEO was announced, effective July 2015.

November 2015: Deutsche Bank penalized for sanctions violations

On 5 November 2015, Deutsche Bank was ordered to pay US$258 million in penalties for doing business with countries under US sanctions.

2015: Lost Share Value

As the share had lost value since mid-2015 and market capitalization had shrunk to around €18 billion, it temporarily withdrew from the Euro Stoxx 50 on 8 August 2016.

2015: Capital Ratio Tier-1 and Job Cuts

In 2015, Deutsche Bank's Capital Ratio Tier-1 (CET1) was reported to be only 11.4%, lower than the 12% median CET1 ratio of Europe's 24 biggest publicly traded banks, so there would be no dividend for 2015 and 15,000 jobs were to be cut.

2015: Loss before income taxes

In January 2016, Deutsche Bank pre-announced a 2015 loss before income taxes of approximately €6.1 billion and a net loss of approximately €6.7 billion.

January 2016: Pre-announcement of 2015 Loss

In January 2016, Deutsche Bank pre-announced a 2015 loss before income taxes of approximately €6.1 billion and a net loss of approximately €6.7 billion.

January 2016: Jain provided consultancy to the bank

Jain's resignation took effect in June 2015, but he provided consultancy to the bank until January 2016.

May 2016: Fitschen continued as joint CEO

Fitschen continued as joint CEO until May 2016.

June 2016: Former employees accused of tax fraud

In June 2016, six former employees in Germany were accused of involvement in a major tax fraud deal with CO2 emission certificates.

2016: Legal Disputes and Litigation Reserves

As of 2016, Deutsche Bank was involved in some 7,800 legal disputes and calculated €5.4 billion as litigation reserves, with a further €2.2 billion held against other contingent liabilities.

2016: No dividend

In 2015, Deutsche Bank's Capital Ratio Tier-1 (CET1) was reported to be only 11.4%, lower than the 12% median CET1 ratio of Europe's 24 biggest publicly traded banks, so there would be no dividend for 2015 and 2016.

2016: One CEO Leads Deutsche Bank

In 2016, Deutsche Bank shifted to being led by one CEO.

2016: Presidential election under scrutiny

In 2016, the U.S. presidential election faced scrutiny regarding potential Russian interference.

2016: Cartel Activities in Europe

In Europe, Deutsche Bank revealed cartel activities in the period between 2005 and 2016 to regulators to receive immunity.

2016: Outstanding loans prior to election

Prior to his 2016 election, Deutsche Bank held more than $360 million in outstanding loans to Donald Trump.

January 2017: Fine Imposed for Anti-Money Laundering Violations

On 30 January 2017, the NYSDFS fined Deutsche Bank $425 million for violating New York's anti-money laundering laws.

May 2017: HNA Group became the biggest shareholder

In May 2017, Chinese conglomerate HNA Group became its biggest shareholder, owning 9.90% of its shares.

December 2017: Mueller investigates Deutsche Bank's role

As of December 2017, Special Counsel Robert Mueller investigated Deutsche Bank's role in Trump and Russian parties allegedly cooperating.

2017: Scheme to Conceal Bribes

In 2017, Deutsche Bank engaged in a scheme to conceal bribes to foreign officials.

2017: Capital Ratio Target

In 2017, Deutsche Bank needed to get its common equity tier-1 capital ratio up to 12.5% in 2018 to be marginally above the 12.25% required by regulators.

2017: FinCEN file leaks

The FinCEN file leaks documented around $1.3 trillion of suspicious transactions through Deutsche Bank between 1999 and 2017.

February 2018: HNA Group's stake reduced

As of February 16, 2018, HNA Group's stake reduced to 8.8%.

March 2018: DWS Group Separated

In March 2018, Deutsche Bank separated the listed asset manager DWS Group (formerly Deutsche Asset Management) from the bank.

July 2018: Deutsche Bank settles improper ADR handling charges

On 20 July 2018, Deutsche Bank agreed to pay nearly $75 million to settle charges of improper handling of American depositary receipts.

November 2018: Police Raid Frankfurt Offices

In November 2018, the bank's Frankfurt offices were raided by police in connection with investigations around the Panama papers and money laundering.

November 2018: Whistleblower links large bank to Danske Bank scandal

On 19 November 2018, a whistleblower stated that a large European bank, allegedly Deutsche Bank's U.S. unit, was involved in helping Danske Bank process $150 billion in suspect funds.

2018: Global Presence and Market Position

As of 2018, Deutsche Bank's network spanned 58 countries with a large presence in Europe, the Americas, and Asia, becoming a component of the DAX stock market index.

2018: Accounts opened with Deutsche Bank

From 2013 to 2018, "Epstein, his related entities and his associates" opened over forty accounts with Deutsche Bank.

2018: CET1 target year

In 2017, Deutsche Bank needed to get its common equity tier-1 capital ratio up to 12.5% in 2018 to be marginally above the 12.25% required by regulators.

February 2019: HNA Group Cutting Stake

In February 2019, HNA Group announced cutting stake in Deutsche Bank to 6.3 percent.

March 2019: HNA Group's Stake Further Reduced

As at March 2019, HNA Group's stake was further reduced to 0.19 percent.

March 2019: Investigation by congressional committees

As of March 2019, Deutsche Bank's relationship with Trump was under investigation by two U.S. congressional committees and by the New York attorney general.

April 2019: House Democrats subpoena the Bank

In April 2019, House Democrats subpoenaed Deutsche Bank for Trump's personal and financial records. On 29 April 2019, U.S. President Donald Trump sued Deutsche Bank to block them from turning over financial records to congressional committees.

May 2019: CEO expects "deluge of criticism"

During the Annual General Meeting in May 2019, CEO Christian Sewing said he was expecting a "deluge of criticism" about the bank's performance and announced that he was ready to make "tough cutbacks" after the failure of merger negotiations with Commerzbank AG and weak profitability.

May 2019: Suspicious transactions detected but not reported

In May 2019, anti-money laundering specialists at Deutsche Bank detected suspicious transactions involving entities controlled by Trump and Kushner, but bank executives rejected recommendations to file suspicious activity reports.

May 2019: Relationship with Jeffrey Epstein continues

Up to May 2019, Deutsche Bank lent money and traded currencies for Jeffrey Epstein, long after his 2008 guilty plea.

June 2019: Job Cuts Announced

In late June 2019, news headlines claimed that Deutsche Bank would cut 20,000 jobs, over 20% of its staff, in a restructuring plan.

July 2019: 1MDB Fraud Scandal Investigation

In July 2019, U.S. prosecutors investigated Deutsche Bank's role in a multibillion-dollar fraud scandal involving the 1Malaysia Development Berhad, or 1MDB.

July 2019: Deutsche Bank Begins Cutting Jobs

On July 8, 2019, Deutsche Bank began to cut 18,000 jobs, including entire teams of equity traders in Europe, the US, and Asia.

October 2019: Bank asserts it does not have Trump's tax returns

In October 2019, a federal appeals court said Deutsche Bank asserted it did not have Trump's tax returns.

December 2019: Court rules Deutsche Bank must release records

In December 2019, the Second Circuit Court of Appeals ruled that Deutsche Bank must release Trump's financial records, with some exceptions, to congressional committees.

2019: Report indicates possible prosecution

In 2019, The Guardian reported that an internal report at Deutsche Bank showed the bank could face fines and prosecution over its role in money laundering.

2019: Raid Conducted on Deutsche Bank

In 2019, a raid was conducted on Deutsche Bank, leading to subsequent investigation.

January 2020: Bonus Pool Cut

In January 2020, Deutsche Bank decided to cut the bonus pool at its investment branch by 30% following restructuring efforts.

July 2020: Deutsche Bank penalized for Epstein connection

On 7 July 2020, the New York Department of Financial Services (DFS) imposed a $150 million penalty on Deutsche Bank, in connection with Jeffrey Epstein.

2020: Reputational Issues

According to a 2020 article in the New Yorker, Deutsche Bank had a long-standing "abject" reputation among major banks due to involvement in major scandals.

2020: End of lending to Donald Trump

By 2020, Deutsche Bank had lent Donald Trump and his company more than $2 billion over twenty years.

2020: Deutsche Bank fined for suspicious transactions

In 2020, Frankfurt-based prosecutors imposed a fine of $15.8 million for Deutsche Bank's failure to promptly report suspicious transactions. Also in 2020, it became known that the U.S. arm of Deutsche Bank processed more than $150 billion of dirty money through New York, for which it was fined 150 million $.

2020: Profit was made

In February 2021, it was reported that Deutsche Bank made a profit of €113 million ($135.6 million) for 2020, the first annual net profit it had posted since 2014.

January 2021: Deutsche Bank Agrees to Pay Fine

In January 2021, Deutsche Bank agreed to pay a U.S. fine of more than $130 million for concealing bribes to foreign officials in countries such as Saudi Arabia and China, and the city of Abu Dhabi, between 2008 and 2017 and a commodities case where it spoofed precious metals futures.

February 2021: Profit Reported

In February 2021, it was reported that Deutsche Bank made a profit of €113 million ($135.6 million) for 2020, the first annual net profit it had posted since 2014.

March 2021: Sale of Holdings Seized from Archegos Capital Management

In March 2021, Deutsche Bank sold about $4 billion of holdings seized in the implosion of Archegos Capital Management in a private deal.

May 2021: Malaysia Sues Deutsche Bank

In May 2021, Malaysia sued Deutsche Bank to recover billions in alleged losses from a corruption scandal at the 1MDB fund.

2021: Deutsche Bank ends relationship with Trump

In early 2021, Deutsche Bank elected to discontinue its relationship with Donald Trump following the January 6 United States Capitol attack.

February 2022: Reference date for depositary receipts

February 2022 is the reference date used in the Deutsche Bank notification about access to shares on depositary receipts.

November 2022: Deutsche Bank sued over Epstein's sex-trafficking operations

On 24 November 2022, two women sued Deutsche Bank for its role in enabling Jeffrey Epstein to run his sex-trafficking operations.

June 2023: Notice regarding access to shares

In June 2023, Deutsche Bank notified customers that it could no longer guarantee them access to shares held on the basis of depositary receipts issued prior to February 2022.

July 2023: DWS Nearing Settlement

In July 2023, the Financial Times reported that DWS (80% owned by Deutsche Bank) was nearing a settlement, having earmarked €21mn for the settlement and incurred €39mn in legal costs.

2023: Deutsche Bank Involved in Anti-Competitive Bond Trading

In 2023, it was revealed that Deutsche Bank was involved in anti-competitive bond trading in UK and EU bonds.

Mentioned in this timeline

Donald John Trump is an American politician media personality and...

Ukraine is a country in Eastern Europe the second-largest on...

Jeffrey Epstein was an American financier and convicted sex offender...

The stock market is where buyers and sellers trade stocks...

Saudi Arabia officially the Kingdom of Saudi Arabia KSA is...

The Guardian is a British daily newspaper founded in as...

Trending

3 hours ago Mojtaba Khamenei Emerges as Central Figure in Escalating Iranian Political Power Struggle

3 hours ago Toronto Raptors Sign Center Trey Jemison to Two-Way Contract

4 hours ago Mike Pence Discusses Future of Conservatism and GOP Populism

4 hours ago Capital One Closes Trump Organization Accounts Over Money Laundering Concerns

4 hours ago Rep. Tom Emmer Faces Serious Health Challenges During Farm Panel Hearing

4 hours ago Madison Keys Faces Antonia Ruzic at WTA National Bank Open in Toronto

Popular

Rand Paul is an American politician and the junior United...

Anthony Stephen Fauci is a prominent American physician-scientist and immunologist...

Lindsey Graham is a prominent American politician serving as the...

Josh Hawley is an American politician and attorney currently serving...

Bernie Sanders is a prominent American politician and the senior...

Jeanine Pirro is an American television host lawyer and author...